Nigeria’s government believes it may have found an opportunity amid global uncertainty. On June 4, 2026, Bloomberg reported the immediate past Finance Minister, Wale Edun, as stating that rising oil prices, improving investor sentiment, and recent sovereign credit upgrades have created conditions that could allow Nigeria to refinance some of its high-cost debt at lower rates,

From the perspective of financial markets, the argument appears persuasive. Sovereign ratings have improved, foreign exchange reforms have been welcomed by investors, and higher oil revenues have strengthened government finances. Yet there is a growing gap between what investors see as economic progress and what many Nigerians experience in their daily lives.

Debt Refinancing May Improve Government Finances, But It Does Not Solve Economic Hardship

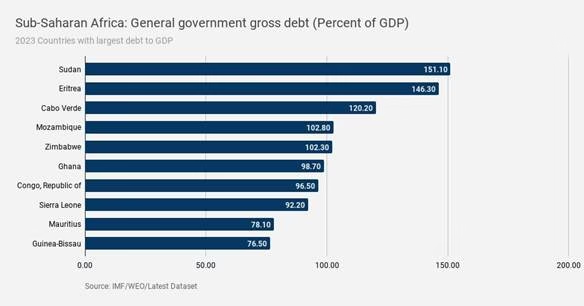

IMF World Economic Outlook Database (Government Gross Debt Data). Nigeria’s debt-to-GDP ratio remains lower than many African peers, but debt sustainability depends on revenue generation and debt-servicing capacity, not debt ratios alone.

Nigeria’s debt burden remains lower than many African countries when measured as a share of gross domestic product. IMF projections for 2026 show that Nigeria remains below the debt levels recorded in countries such as Egypt, South Africa, Zambia, Sudan, and Mozambique (IMF World Economic Outlook Database). This finding is also reflected in comparative African debt analysis showing Nigeria and the Democratic Republic of Congo below 40 percent debt-to-GDP, while several African economies exceed 70 percent and some exceed 100 percent (Africa’s Debt and Remittance Costs Are Quietly Draining the Continent, attached document, pp. 1-2).

Government officials frequently use these comparisons to argue that Nigeria’s debt remains manageable. However, debt sustainability is not determined solely by debt-to-GDP ratios. What ultimately matters is whether a country can generate sufficient revenue to service its obligations while still funding healthcare, education, infrastructure, and social welfare.

Across Sub-Saharan Africa, rising debt-service obligations are increasingly limiting governments’ ability to invest in development priorities, forcing many countries to devote larger shares of public revenue to debt repayment rather than public services, as reported by the IMF for Fiscal Monitor on Africa’s Debt and Remittance Costs Are Quietly Draining the Continent.

Refinancing debt may reduce future borrowing costs, but it does not automatically create jobs, reduce poverty, lower inflation, or improve living standards. It changes the terms of repayment rather than addressing the deeper economic challenges confronting ordinary citizens.

Credit Upgrades Are Not the Same as Economic Well-Being

Nigeria has received increasing praise from international investors and credit rating agencies. S&P Global Ratings recently upgraded Nigeria’s sovereign rating, citing improvements in oil production, exchange-rate liberalization, and expanding domestic refining capacity linked to the Dangote Refinery (Reuters coverage cited in Credit Upgrades and Nigeria’s Economic Reality). Yet these indicators measure investor confidence rather than household welfare.

According to the World Bank, more than 60 percent of Nigerians are estimated to live below the national poverty line, while approximately seven million additional Nigerians fell into poverty during 2025, as reported by the World Bank. Similar concerns have been highlighted in analysis of Nigeria’s recent reforms, which notes that poverty and food insecurity remain severe despite improvements in macroeconomic indicators.

The IMF Country Analysis and Reform Assessments on the International Monetary Fund has likewise acknowledged that while reforms are beginning to improve fiscal and monetary stability, poverty and food insecurity remain elevated (IMF Country Analysis and Reform Assessments.

The disconnect is increasingly difficult to ignore. Fuel subsidy removal contributed to significant increases in petrol prices, transportation costs, electricity tariffs, and food prices, while naira depreciation increased the cost of imported goods and essential commodities (Credit Upgrades and Nigeria’s Economic Reality).

As a result, many Nigerians find discussions about sovereign ratings, bond yields, and investor confidence disconnected from everyday concerns such as food affordability, transportation expenses, and declining purchasing power. A country can receive international praise while its citizens continue to struggle economically. These realities are not contradictory. They are occurring simultaneously in Nigeria today.

The Real Measure of Success Is Whether Nigerians Feel the Benefits

The broader African context offers another perspective on the debt debate. While governments across the continent continue borrowing to finance development, households and diaspora communities continue losing billions of dollars through expensive remittance systems.

According to the World Bank’s Remittance Prices Worldwide database, remittance costs remain among the highest globally in several African corridors. Analysis based on World Bank data shows that sending $200 to Nigeria costs approximately $5.07 in fees, while some African countries face dramatically higher costs. Malawi, for example, incurs fees exceeding $43 for the same transfer amount.

This reveals a deeper contradiction. African governments increasingly seek external financing while substantial financial resources are lost through inefficient remittance systems. Instead of fully harnessing diaspora capital, significant portions are absorbed by transaction costs (Africa’s Debt and Remittance Costs Are Quietly Draining the Continent).

The same contradiction is visible in Nigeria’s debt refinancing discussion. Edun argued that stronger oil revenues and improved investor sentiment have created favorable financing conditions. Investors may well agree. But ordinary Nigerians are asking a different question.

Recent debate surrounding Nigeria’s debt profile reflects growing frustration that improvements in debt sustainability, sovereign ratings, and investor confidence have not yet translated into lower living costs or better living standards (Nigeria’s Debt Debate Reflects a Wider Struggle Between Economic Stability and Public Hardship).

Conclusion

As broadcaster Rufai Oseni argued during a recent public discussion, citizens are concerned not simply about the size of government debt but about whether public revenues are increasingly being consumed by debt servicing while social needs remain unmet.

The government may succeed in reducing borrowing costs. Investors may continue rewarding reforms. Credit agencies may issue additional upgrades. But the ultimate measure of economic success is not whether creditors feel more comfortable lending to Nigeria. It is whether Nigerians themselves become better off. Until lower inflation, stronger job creation, improved security, rising incomes, and greater affordability become visible in everyday life, debt refinancing will remain a financial achievement that many citizens struggle to celebrate. It is to be seen what the current Minister of Finance and Coordinating Minister of the Economy, Taiwo Oyedele, would do differently to change the narrative.